6 lessons for helping youth build financial literacy

Thokozani Chikuni-Ziwa and Jamie Walsh

Financial literacy plays several important roles in economic development: it helps individuals manage their money better, promotes entrepreneurship and financial inclusion, enhances consumer protection, and even supports financial stability.

But can financial education also reduce youth depression and anxiety?

That is the question being asked by the Shamiri Institute, a data-driven social venture that trains 18-to-22 year-olds in Africa to deliver effective and community-based group therapy. In a recent RCT, Shamiri discovered something surprising: the study’s control group – which did not participate in therapy but did receive basic life-skills training – experienced strikingly reduced symptoms of anxiety and depression.

To further test and understand this finding, Shamiri (a grantee with The Agency Fund) is developing a non-therapy intervention that focuses on helping youth build highly relevant life skills, including a module on how to deal with financial problems – i.e., budgeting, saving, and strategies for earning money.

On April 9, Shamiri and The Agency Fund co-hosted a workshop to help the organization inform the contents of its financial education module. The event featured academics, practitioners, and experts to review recent innovative studies on youth financial literacy and identify key lessons and insights from the field.

How to help youth in the global south build financial literacy

After an introduction by Research Manager Brenda Ochuku about Shamiri’s recent findings and goals for its financial education module, the event featured presentations by four experts and practitioners: Miriam Bruhn, Senior Economist in the Finance and Private Sector Development Team World Bank; Julian Jamison, Professor of Economics and Senior Research Fellow at the University of Oxford/University of Exeter; Meghan Mahoney, Global Director of Research, Measurement, and Evaluation at Educate!; and Margaret Miller, an Expert Consultant and former World Bank Global Lead for Responsible Financial Access.

Overall, the participants underscored that youth financial literacy is a highly promising intervention, but that how programs are designed and implemented matters greatly:

“Financial education can have an impact,” said Miller, who presented findings from a 2014 meta-analysis of 188 financial education interventions that showed an overall positive impact on savings behavior. “Part of the problem is that they’re often very short, small, and not necessarily well-developed interventions – and those don’t have an impact.”

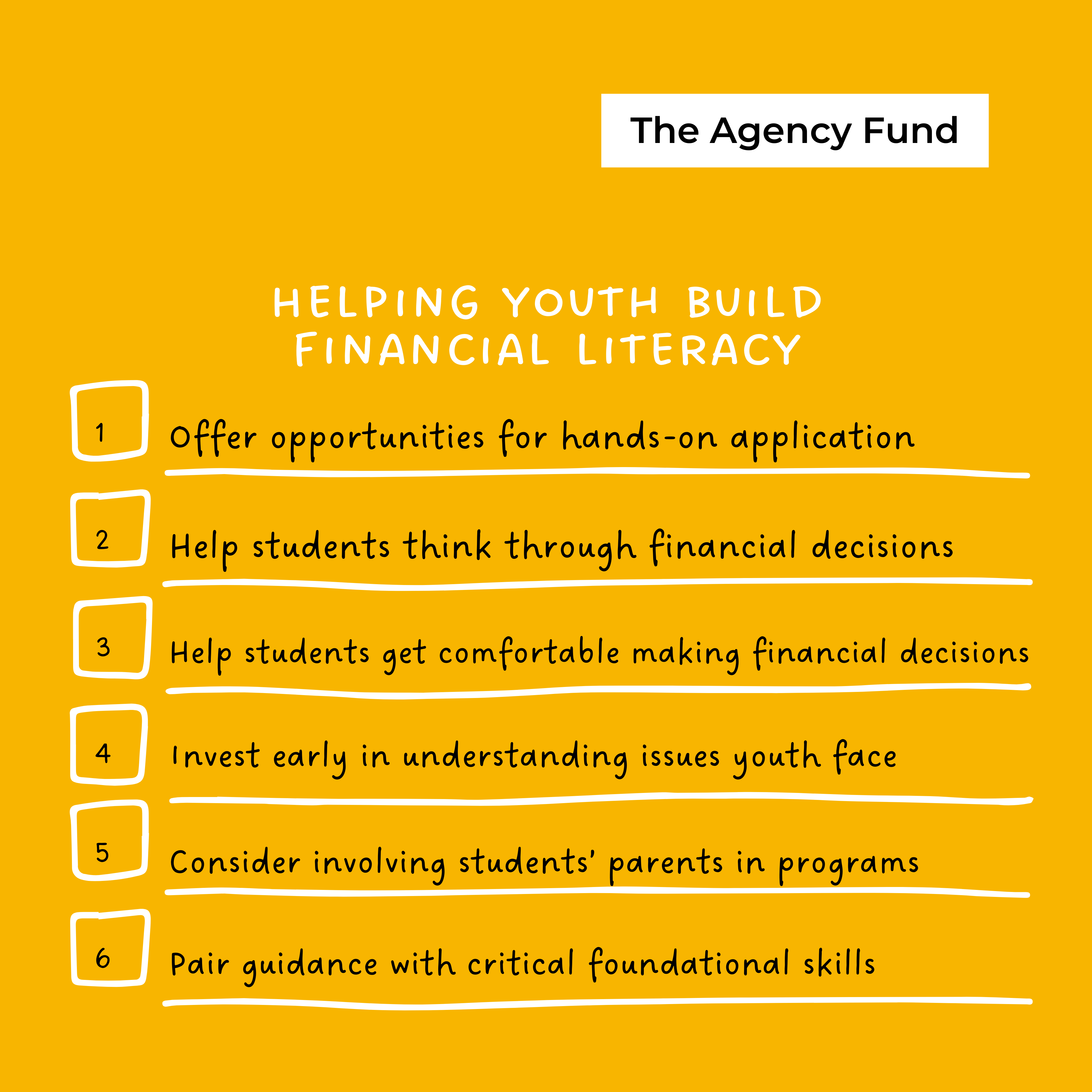

The presenters highlighted six key lessons for designing financial literacy interventions:

1. Offer opportunities for hands-on application

The discussion emphasized the need for practical, realistic, and hands-on financial education exercises that relate directly to students’ lives and encourage them to apply the lessons outside the classroom. For example, an exercise on budgets could focus on the need to save money for school fees while highlighting the difference between needs and wants.

“Hands-on practical application is key,” said Mahoney, whose organization Educate! combines financial literacy skills training, mentorship, and practical entrepreneurship experience for youth in Kenya, Rwanda, and Uganda. “We think about how to do this in the context of a classroom for a lesson, but also making it real and drawing a link to outside the classroom, when you’re out in the world practicing and applying it. That’s the thing that is actually going to make these skills stick.”

2. Help students think through bigger financial decisions

Effective financial education seeks to help students understand the types of financial decisions that they will likely encounter in their lives, then give them tools to effectively navigate those decisions.

“Use material that is relevant to the students,” said Bruhn, who presented findings from a study that found positive impacts from a comprehensive financial education program in Brazil involving nearly 900 high schools and approximately 25,000 students. “Buying a computer, for example: do you really need the computer? If you decide to buy it, how do you research the options? How do you finance the options? Are you going to save for it, or are you going to get credit for it? Think through examples that are really relevant for the students.”

3. Develop comfort with the practice of financial decision-making

Financial literacy is about more than basic math, finance, and accounting – it’s a process of learning-by-doing and ensuring that students are both prepared to earn and save money but also overcome financial challenges when they arise.

“It’s not ‘knowledge,’ per se – it’s not about interest rates and banks,” said Jamison, who discussed a program that offered financial education and subsidized group savings accounts to youth in Uganda, with positive impacts on savings and income for all treatment arms at both one year and five years. “It’s knowing that financial issues are important and knowing that resources are available when you want them, so you will be able to use them in real time.”

4. Understand the issues your students are facing

Participants also underscored the importance of understanding your students’ unique challenges and how financial literacy interacts with those issues. They discussed the psychological and social pressures that students often face and that could impact their financial decisions, such as the desire to keep up with peers – an issue that could potentially be addressed by working with school administrators to foster cultures that discourage ostentatious spending.

“The key thing is to really understand the youth market that you’re working with and the issues that they’re having and facing – in as relevant and immediate a way as possible,” said Miller, who also highlighted the possibility of exploring community examples of "positive deviance" (i.e., households that manage their finances successfully despite having similar incomes to others who struggle) to generate insights about effective strategies that could be taught to others.

5. Consider involving students’ parents, if relevant

The discussion highlighted the value of thinking about financial education beyond the students themselves and involving the wider community, including parents and teachers, to reinforce key lessons, skills, and strategies.

“There is a real opportunity to involve the parents, because the parents are also likely to have quite low financial literacy,” said Bruhn. “If you can reach the student, you can have the student be an agent of change in the household.”

6. Pair guidance with critical foundational skills

Ultimately, however, effective financial education ensures that students internalize key foundational skills.

“You have to understand the context that the youth are operating in, but there is a sort of minimal foundation,” said Mahoney. “No matter what numeracy skills a student comes into the program with, you want them to be able to calculate a profit at the end of the day. For it to be effective and actually translate into long-term impacts in students' lives, it has to be paired with critical transferable skills – just thinking about building financial literacy on its own is probably not going to move the needle.”

Looking ahead

In the near-term, the insights gathered from the event provided the Shamiri Institute with valuable inputs for designing their financial skills module – which they plan to roll out later this year, starting in Nairobi. More broadly, the event offered important lessons for any organization seeking to enhance financial literacy in the global south. To be effective and impactful, financial education programs should strive to ensure that they are practical, applicable, and supportive of students’ real financial challenges.