As a philanthropic advisor, I’ve had the good fortune to be involved in a committed effort to fund cost-effective poverty alleviation. In this post I’d like to share one aspect of the learning journey, which I hope will be valuable to others pushing for progress on poverty and other challenging social outcomes. It also illustrates how we make investment decisions at The Agency Fund.

There was a time when the most common pitch to poverty funders went something like this: Hundreds of millions of impoverished entrepreneurs in the world are credit constrained – commercial banks won’t lend them money. But they have attractive investment opportunities at their disposal (multiplying goats! emerging markets!). If somebody only took a chance on them, they could generate income and return the funds with interest. And a nonprofit lender who recycles these funds can get a flywheel going that keeps on giving until poverty is eradicated for good. This was a compelling story for donors who had capital and wanted to reduce poverty; many (my clients included) invested liberally in microcredit nonprofits.

Over time, questions emerged. Which grantees were accomplishing what in the way of poverty reduction? What returns did their borrowers achieve on their investments, and how did that compare to the interest rates on their loans? To which organizations should we allocate funding to maximize poverty reduction, and to whom should these organizations allocate loans? To answer these questions, my clients started to shift about half of their microcredit contributions toward learning and evaluation.

As evidence accumulated, the results were sobering. Most borrowers did not appear to channel their loans into profitable investments. In fact, the average amount of poverty reduction was indistinguishable from zero. Although this was certainly disappointing, we as a field did learn from these experiences. My clients expanded their poverty grantmaking beyond microcredit, and a few grantees tried to micro-target their lending to users who were more likely to benefit.

Then something interesting happened with the evaluation findings: they contributed to a broader body of evidence that seemed to “change the narrative,” well beyond the grantees and us. The false promise of a silver bullet evaporated; meanwhile, a productive field of research emerged to better understand who can make good use of which types of loans, and under what conditions. The capital allocations of third parties, including major development organizations, started to shift, sometimes with explicit reference to evidence. Buoyed by this, we continued to invest in research and policy translation (ultimately, well beyond microcredit).

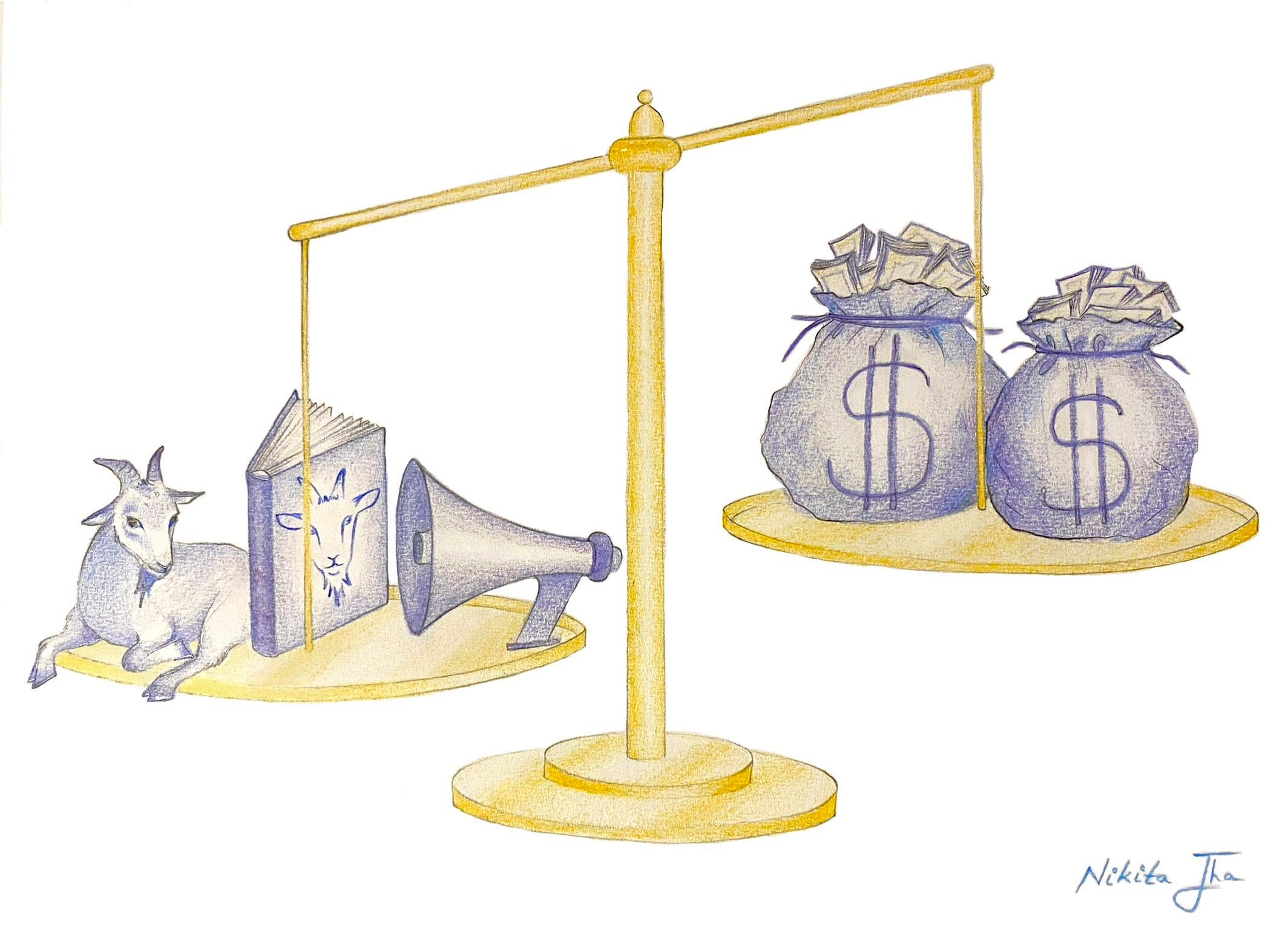

After the fact, the “return on investment” seems to have come mainly from the public goods nature of the research. But this was not foreseeable at the outset – or was it? Well, while we didn’t foresee the research results, we could have been more clear-eyed about three “potential” sources of value:

🐐 Direct value: The impact of expanding the scale of a program.

📚 Learning value: The value of (yet-undiscovered) insights that may improve the capital allocation of the implementer and/or donor in the future.

📣 Leveraged value: The potential to help improve the capital allocation of major third parties.

In retrospect, rather than meandering with a limited aperture from programming to evaluation to research, we would have been well advised to deliberately account for all potential sources of value at the outset, and then maximize them jointly. It is possible to seek impacts right away, while simultaneously using rigorous evaluation protocols to learn about potential adjustments, and trying to anticipate which lessons might prove useful to third parties down the road.

Today, when we appraise a potential investment at The Agency Fund, we consider direct value, learning value, as well as leveraged value. Some of our most compelling grantees also focus on all three: they perform an intervention to have direct impact, they learn how to become even more impactful in the future, and they aspire to maximize the value of these insights beyond their own programming. These three factors directly map to our goal of promoting an ecosystem of players that have an implementation muscle, a learning muscle, and a policy lever.